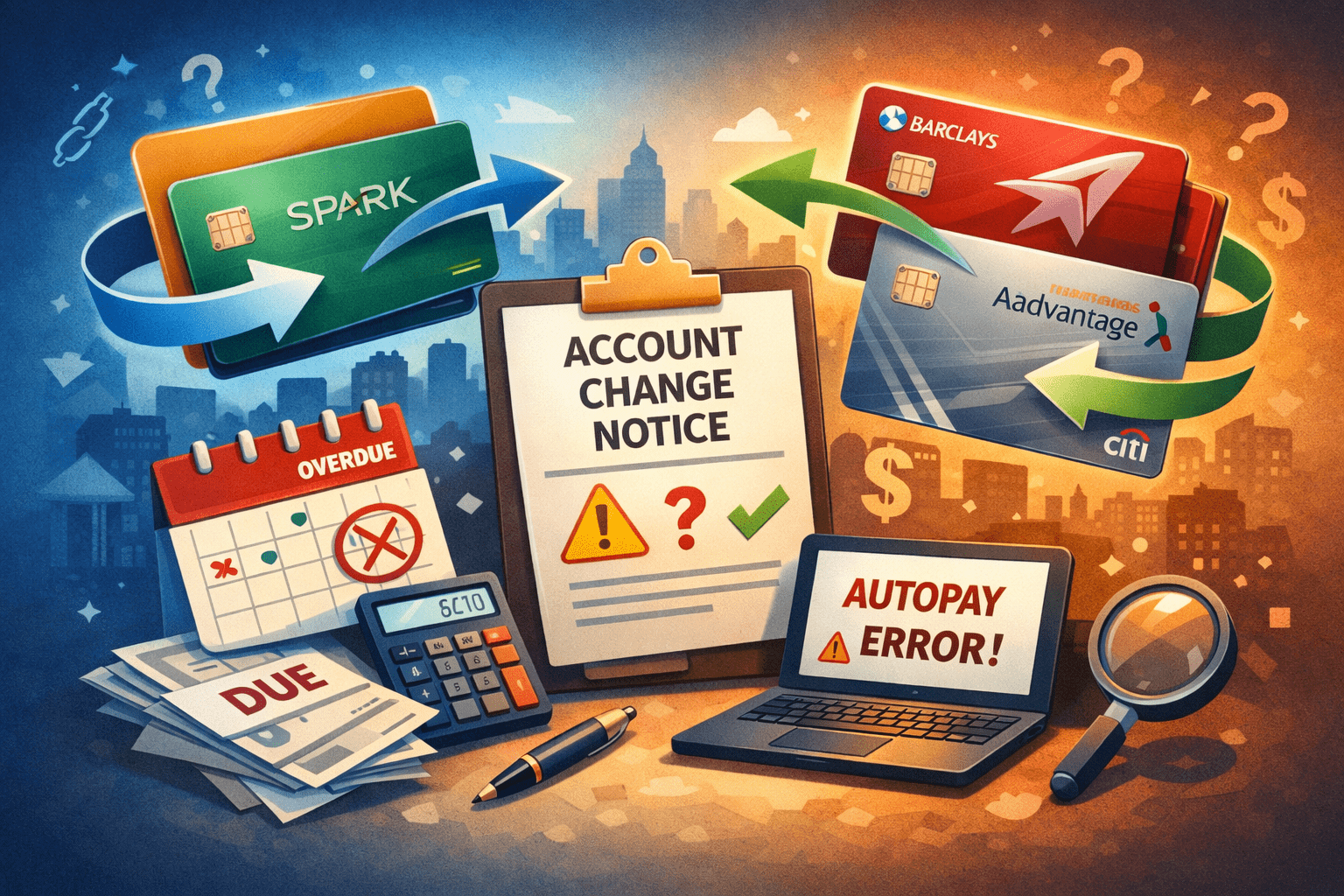

Card replacements like Barclays Aviator → Citi or “my Discover card became a Capital One card” aren’t just annoying — they can quietly disrupt your cash flow, bookkeeping, and even your vendor relationships.

The “Wait…this isn’t my card anymore” problem

If you’ve ever opened your mailbox and thought:

- “Why is my Barclays Aviator becoming a Citi Aviator?”

- “Why did my Discover business card turn into a Capital One Spark?”

- “Did I get hacked…or is this legit?”

You’re not alone. And no — it’s not automatically fraud.

In many cases, what you’re seeing is the behind-the-scenes business of banking: mergers, portfolio sales, and co-brand contract changes. The plastic changes, the bank name changes, sometimes the rewards change — but your day-to-day risk is simpler:

Recurring charges fail, autopay breaks, and accounting gets messy.

Let’s walk through what’s going on and what you should do next.

The big reasons credit cards get “re-homed”

1) Co-branded partnerships get renegotiated (airlines, hotels, retailers)

This is the cleanest explanation for the AAdvantage Aviator change.

American Airlines and Citi expanded their co-branded credit card relationship, and Citi is expected to become the exclusive issuer of AAdvantage co-branded cards in the U.S.

That’s why multiple sources report that Barclays-issued Aviator cardholders will be transitioned to Citi-issued AAdvantage cards starting April 24, 2026.

Translation: your card didn’t “change” because you did something wrong — the partnership structure changed.

2) Mergers create product overlap (and banks simplify)

Capital One and Discover merged into one company (Capital One, N.A.).

When large issuers combine, they eventually:

- unify systems (logins, statements, servicing),

- reduce redundant products,

- migrate portfolios to the “winning” platform.

Capital One’s own FAQ tells customers they’ll be notified as updates roll out.

Some customers have reported being moved onto Capital One systems, and a few report product conversions. Since public “conversion tables” aren’t consistently posted in official channels for every niche product, the best approach is to treat any replacement as a standard conversion event and take the protective steps below.

“How many people is this happening to?”

For the AAdvantage Barclays → Citi change, the public guidance indicates this is a portfolio-wide transition for existing Barclays AAdvantage cardholders, with a firm transition date widely reported.

For the Capital One–Discover side, we do have scale indicators from deal materials describing a franchise of 100+ million customers across the combined companies (that’s customers overall, not “cards converting this month,” but it shows why migrations can surface everywhere).

The practical takeaway is this:

Even if your specific card is “rare,” the forces driving these changes are affecting huge numbers of consumers and businesses.

The CPA at Large “Do This Now” Checklist (so nothing breaks)

Step 1: Protect your cash flow first (recurring charges & autopay)

Make a quick list of everything that charges that card automatically, especially:

- web hosting, SaaS tools, email platforms

- insurance

- utilities

- subscriptions (business + personal)

- ad platforms (Meta/Google)

- toll tags, parking apps

- any vendor that locks accounts if a payment fails

Action:

- Log in and update the card on file anywhere mission-critical.

- Set calendar reminders for the next two billing cycles to confirm charges succeed.

Pro tip: autopay failures often show up 2–6 weeks later — right when you’ve forgotten the card ever changed.

Step 2: Download your statements BEFORE you lose access

Portfolio transfers can come with login changes or “old portal shutdown” windows.

Action:

- Download the last 12–24 months of statements (PDF) and year-end summaries.

- Save them to your tax folder (by year).

If you’re ever audited, disputing a charge, or proving a business expense, having the statements already saved is priceless.

Step 3: Expect the card number to change (but the account history may continue)

Many transitions include:

- new physical card

- new card number and security code

- sometimes a new “issuing bank” on your credit report

Action:

- Update payment vaults (Amazon, PayPal, Apple Pay/Google Wallet, etc.)

- Update vendors who store your card (especially ad platforms and hosting)

Step 4: Bookkeeping cleanup (QuickBooks and receipts)

If you run bookkeeping (or you’re the one who inevitably “becomes the bookkeeper”), a card swap can cause:

- duplicated bank feeds

- broken rules

- confusion when transactions start coming from a new issuer name

Action in QuickBooks Online (simple version):

- Keep the old card feed connected until you confirm it’s truly inactive.

- If a new feed appears, label it clearly (e.g., “CapOne Spark (Former Discover)”).

- Use memo/rules carefully until you see a full month of transactions.

Step 5: Watch for “silent” benefit changes

Even when the card looks “equivalent,” details can change:

- travel protections

- multipliers

- companion certificates

- annual fee timing

- redemption rules

For the AAdvantage move, reporting indicates cardholders are being transitioned to Citi equivalents as Citi becomes the exclusive issuer.

Action:

- Compare the benefit guide you used to have with the new one.

- If you relied on a specific benefit, confirm it still exists before you plan travel around it.

Red flags (when you should slow down)

A legitimate transition usually comes with:

- multiple notices (email + mail),

- clear timelines,

- official customer service numbers,

- “no action needed” language plus specific action items (like updating your address).

If you get a “replacement card” notice that asks for:

- your full SSN via email,

- a weird link,

- gift cards or wire transfers,

…treat it as phishing.

Bottom line

Card transitions are becoming more common because:

- big-bank consolidation is real,

- co-branded deals are getting reshuffled,

- and banks are simplifying product lineups post-merger.

The best response isn’t panic — it’s process.

If you do the checklist above, you’ll avoid the real damage: failed payments, late fees, and messy books.